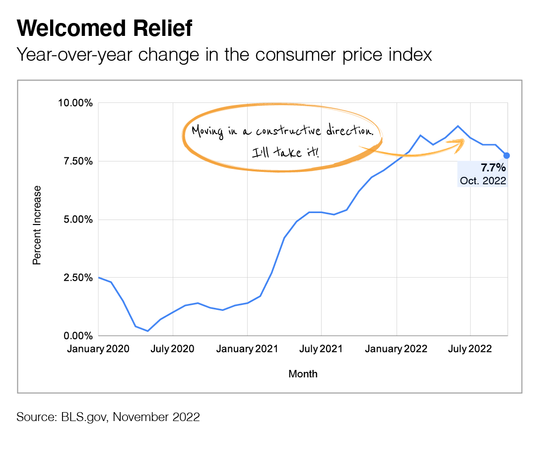

Mortgages in Retirement

Anyone who has gone through the process of mapping out their retirement knows there can be a lot to keep in mind. Saving, investing, anticipating medical costs, and making sure you have enough tucked away for years to come is just the start. One question many people overlook is: “Should I pay off my mortgage before I retire?” The answer is more complicated than you may think.

Opportunity Cost

Imagine you have $300,000 set aside to pay off your mortgage. But rather than using those funds to pay off your mortgage, you instead invest that money. Sure it’s tempting to stop making a monthly payment, but what if that $300,000 earned a hypothetical 6% for the next five years. You would have a little more than $400,000. Yes, your house may appreciate in value over the same period of time, but you should consider all your choices for that lump-sum of money.1

Eradicate (Other) Debt

Before you pay down your mortgage, any extra cash might be better suited to paying off other kinds of debt that carry higher interest rates, especially non-deductible debt, such as credit card balances.2

Make Your Mortgage Work

Some homeowners benefit from a mortgage interest deduction on their taxes. Here’s how it works: the amount you pay in mortgage interest is deducted from your gross income, which reduces your federal income tax burden. But remember, the further along you are toward paying off your mortgage, the less interest you’re paying. If you’re unsure if you’ll be able to take advantage of this mortgage benefit, it’s best to consult your financial professional.3,4

Retire Your Mortgage

Don’t Throw Your Money Away

Your monthly mortgage payment may be a large part of your available capital, especially in retirement. Eliminating unnecessary subsidies can significantly reduce the amount of cash you need to meet monthly expenses.

Uninteresting Interest

Depending on the length of your mortgage term and the size of your debt, you may be paying a substantial amount in interest.

“Paying off your mortgage early can free up money for other uses.”

True, you may lose the mortgage interest tax deduction, but remember as you get closer to paying off your loan: more of each monthly payment goes to principal and less to interest. In other words, the amount you can deduct from taxes decreases.5

Home Is Where the Heart Is

There’s a value to your home beyond money. It’s where you raised your children, made fond memories, and you may want it to remain in the family. Paying off the mortgage may help make your home part of your legacy. Afterall, some things you just can’t put a price on.

1. This is a hypothetical example used for illustrative purposes only. It is not representative of any specific investment or combination of investments. Investments seeking to achieve a higher rate of return also involve higher risks. You should consider your risk tolerance before committing to any investment strategy.

2. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation.

3. Investopedia.com, 2021. Under the 2017 Tax Cuts and Jobs Act, mortgage interest deductibility is limited to mortgages up to $750,000 ($375,000 if married filing separately) in principal value. This article is more informational purposes only, and is not a replacement for real-life advice. Please consult a tax, legal and accounting professional before modifying your tax strategy.

4. IRS.gov, 2022

5. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG Suite is not affiliated with the named broker-dealer, state- or SEC-registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Copyright 2022 FMG Suite.

Dr. Jason Van Duyn

Dr. Jason Van Duyn

586-731-6020

AQuest Wealth Strategies

President

Dr. Jason Van Duyn CFP®, ChFC, CLU, MBA is a Registered Representative with and Securities and Advisory Services offered through LPL Financial, a Registered Investment Advisor. Member FINRA & SIPC. The LPL Financial registered representative associated with this site may only discuss and/or transact securities business with residents of the following states: IN, IL, TX, MI, NC, AZ, VA, FL, OH and CO.

Dr. Jason Van Duyn CFP®, ChFC, CLU, MBA is a Registered Representative with and Securities and Advisory Services offered through LPL Financial, a Registered Investment Advisor. Member FINRA & SIPC. The LPL Financial registered representative associated with this site may only discuss and/or transact securities business with residents of the following states: IN, IL, TX, MI, NC, AZ, VA, FL, OH and CO.