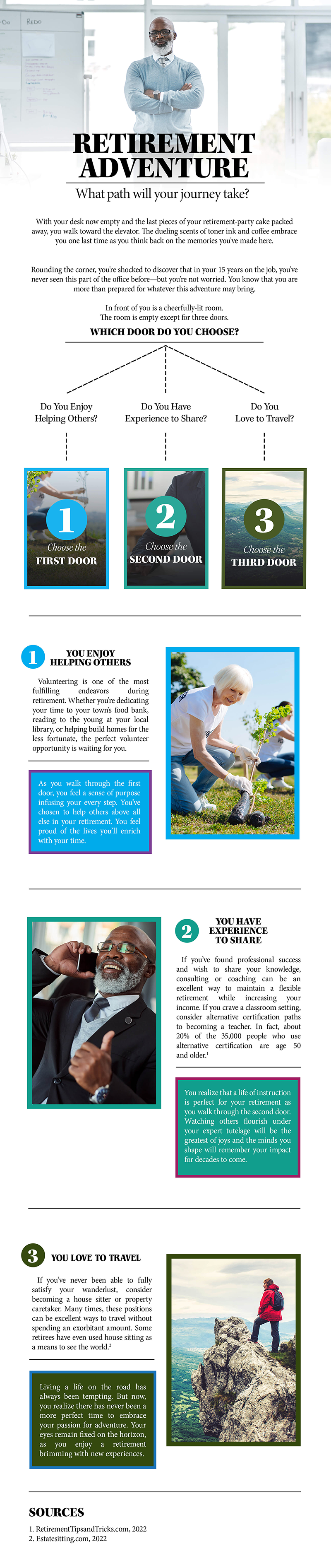

Retirement Realities

Expectations vs. Reality

Predicting exactly what your retirement will be like is about as possible as a meteorologist predicting the weather correctly every single time. In fact, few retirees find their financial futures playing out precisely as they assumed. But, understanding some of the more common assumptions about retirement may help you get closer to your goal than most.

Do retirees actually “outlive” their money?

Generations ago, as people retired, many did live in dire straits, sometimes “down to their last dime,” which lead to the creation of Social Security. Today, Social Security is still around and a common supplement to one’s retirement strategy. True, health crises can sometimes impoverish retirees, but working with a financial professional may even help you prepare for this hard-to-anticipate cost.

Retiring on 70-80% of your end salary may not be feasible

A quick internet search reveals all sorts of sources instructing new retirees should strive to retire on 70-80% of their end salary, but it can be a tough one to achieve.

Most new retirees often want to travel, explore new pursuits, learn some hobbies, and finally get around to those things they had put off when they were too busy with work. So, in the first few years, some may spend roughly as much as they did before retirement.

For many retirees, median household spending increases on the way to a retirement transition. But, with a smart financial strategy, the annual median household spending in retirement tends to decline gradually after age 65.1

Practice makes perfect, even in retirement

On average, households headed by those older than 65 spend 25% less annually than younger households (a difference of more than $15,000). While health care spending increases in retirement, other household costs decline, particularly transportation and housing expenses.2

Retirement may arrive earlier than expected

Most people retire closer to age 60 than age 70. Believe it or not, the average retirement age in this country is 65 for men and 63 for women. That means you could find yourself claiming Social Security earlier than you expected if only to avert drawing down your retirement savings too quickly.3

Living the life you want

In general, American retirees seem to have it pretty good. A recent survey found that 7 in 10 retirees are confident they will have enough money saved to live comfortably throughout retirement.4

Remain flexible in retirement

Your retirement may differ slightly or even greatly from the retirement you have imagined. Fortunately, it may be possible to create a flexible retirement strategy with the help of a financial professional. It’s never too late to start!

Dr. Jason Van Duyn

Dr. Jason Van Duyn Dr. Jason Van Duyn CFP®, ChFC, CLU, MBA is a Registered Representative with and Securities and Advisory Services offered through LPL Financial, a Registered Investment Advisor. Member FINRA & SIPC. The LPL Financial registered representative associated with this site may only discuss and/or transact securities business with residents of the following states: IN, IL, TX, MI, NC, AZ, VA, FL, OH and CO.

Dr. Jason Van Duyn CFP®, ChFC, CLU, MBA is a Registered Representative with and Securities and Advisory Services offered through LPL Financial, a Registered Investment Advisor. Member FINRA & SIPC. The LPL Financial registered representative associated with this site may only discuss and/or transact securities business with residents of the following states: IN, IL, TX, MI, NC, AZ, VA, FL, OH and CO.