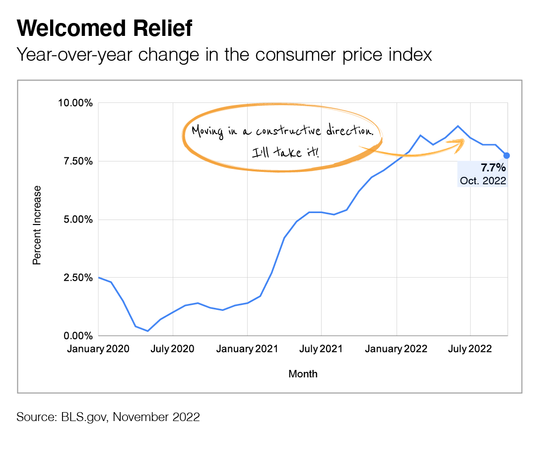

October CPI: Game Changer or Head Fake?

October’s Consumer Price Index (CPI) had some encouraging news for investors, but others asked, “Is this a game changer or another head fake?”

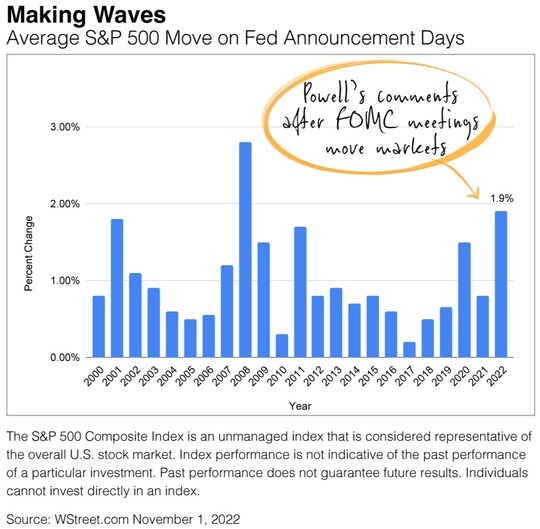

While it’s a bit early to know the answer, it was great to see that inflation rose at a slower-than-expected rate in October. The financial markets welcomed the report as investors hoped the news might influence the Fed’s decision about future rate adjustments.

Fed Chair Powell knows that few financial events can be as devastating as high inflation over time – especially for those living on a fixed income. So, the Fed has been committed to raising short-term rates this year to slow the economy and, in turn, slow inflation.

So, if you held my feet to the fire, would I say the CPI report was a game changer or a head fake? Well, I’m 100% optimistic that the Fed is committed to managing inflation and the current CPI trend appears to be moving in a constructive direction.

Dr. Jason Van Duyn

Dr. Jason Van Duyn

586-731-6020

AQuest Wealth Strategies

President

Dr. Jason Van Duyn CFP®, ChFC, CLU, MBA is a Registered Representative with and Securities and Advisory Services offered through LPL Financial, a Registered Investment Advisor. Member FINRA & SIPC. The LPL Financial registered representative associated with this site may only discuss and/or transact securities business with residents of the following states: IN, IL, TX, MI, NC, AZ, VA, FL, OH and CO.

Dr. Jason Van Duyn CFP®, ChFC, CLU, MBA is a Registered Representative with and Securities and Advisory Services offered through LPL Financial, a Registered Investment Advisor. Member FINRA & SIPC. The LPL Financial registered representative associated with this site may only discuss and/or transact securities business with residents of the following states: IN, IL, TX, MI, NC, AZ, VA, FL, OH and CO.