How You Can Purchase I Bonds Direct from the Treasury

With inflation hovering near 40-year highs, some investors are looking for investments that keep pace with rising prices. For many, a Series I Savings Bond is just the ticket. I Bonds give investors a rate of return plus inflation protection and are backed by the U.S. government.

It’s been big business. The Treasury sold more than $27 billion of I Bonds since last year. That’s more than a 70-fold increase from 2020, when inflation hovered in the 1 percent range.1

Purchasing I Bonds through Treasurydirect.gov is simple. In fact, the site was recently redesigned, making now an excellent time to give it a look.2

Here’s how to get started.

1. Gather your info. Make sure you have the following close at hand: your taxpayer identification number, current address, checking or savings account information, and email address.

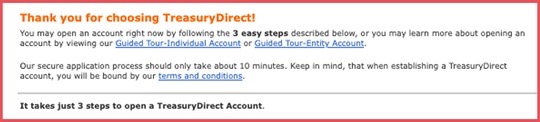

2. Go to Treasurydirect.gov’s account creation page. Navigate to the bottom of the page and select “Apply Now” on the left. This will begin your account creation journey. Next, you will choose between an Individual or Entity account. Select the Individual account type (the default option) and click “Submit.”

3. Enter your info. Using the information gathered in step 1, fill in the fields requested and check the box at the bottom to certify your Taxpayer Identification Number. Click “Submit.

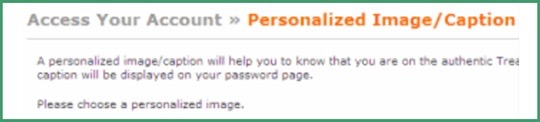

4. Select a personalized image. Take some time here to select an image and caption you will remember. Think of this as a visual password for your account. Click “Submit.”

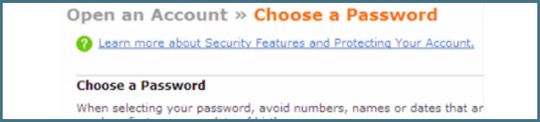

5. Secure your account. Select your password and security questions on this screen. Make sure the answers to your security questions are impossible to guess but easy to remember. Click “Submit” to move to the final step.

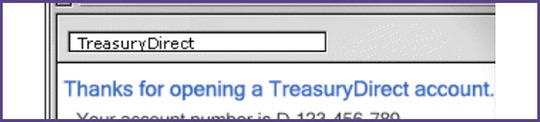

6. Check your email. Finally, look for your TreasuryDirect account number in your email. You’ll need this to log into your account later.3

You can begin purchasing I Bonds now that you’ve created your account. Here are a few things to keep in mind. I Bonds earn interest for 30 years unless you cash them in. You can do this after a year has passed from the time of purchase, but you’ll lose the previous three months of interest. However, if you let them mature for five years or more, there is no penalty.

The maximum amount you can invest is $10,000 per person per year. A married couple can buy up to $20,000. Parents can create custodial accounts for children and then make a purchase. A person can invest up to $15,000 if they elect to get tax refunds in I Bonds.4

Questions about I Bonds or anything else financial? Feel free to reach out anytime.

Dr. Jason Van Duyn

Dr. Jason Van Duyn

586-731-6020

AQuest Wealth Strategies

President

Dr. Jason Van Duyn CFP®, ChFC, CLU, MBA is a Registered Representative with and Securities and Advisory Services offered through LPL Financial, a Registered Investment Advisor. Member FINRA & SIPC. The LPL Financial registered representative associated with this site may only discuss and/or transact securities business with residents of the following states: IN, IL, TX, MI, NC, AZ, VA, FL, OH and CO.

Dr. Jason Van Duyn CFP®, ChFC, CLU, MBA is a Registered Representative with and Securities and Advisory Services offered through LPL Financial, a Registered Investment Advisor. Member FINRA & SIPC. The LPL Financial registered representative associated with this site may only discuss and/or transact securities business with residents of the following states: IN, IL, TX, MI, NC, AZ, VA, FL, OH and CO.

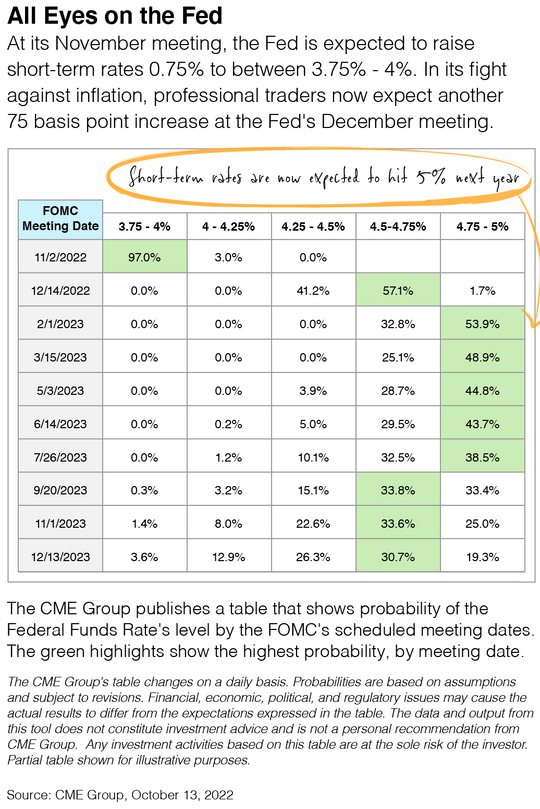

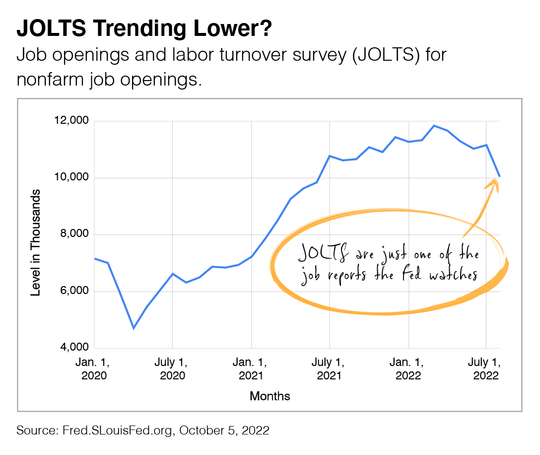

The Fed is looking for three key things in its fight to stabilize the economy. A slowed Gross Domestic Product (GDP), inflation as measured by the Consumer Price Index to fall, and the labor market to soften. Now, GDP has already slowed, but as we all know, inflation has yet to be tamed, and the labor market is mixed at best.

The Fed is looking for three key things in its fight to stabilize the economy. A slowed Gross Domestic Product (GDP), inflation as measured by the Consumer Price Index to fall, and the labor market to soften. Now, GDP has already slowed, but as we all know, inflation has yet to be tamed, and the labor market is mixed at best.