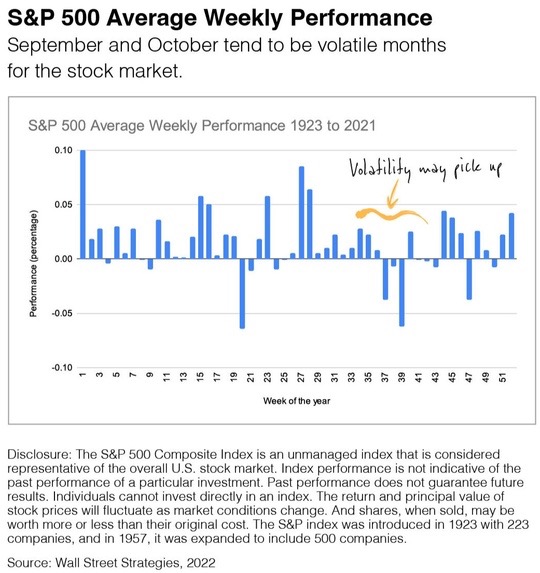

These Months are More Volatile Than Others

We’re entering a tricky time of year: September and October have a reputation for bringing an extra measure of market volatility.

Some of the stock market’s most challenging events have hit in September and October, and other seasonal trends can also play a part. Investopedia found that institutions start preparing for year-end distributions around this time. Plus, individuals tend to reposition their portfolios after the summer months.

This chart shows the average weekly S&P 500 performance since 1923. I’ve highlighted September and October so you can see how they compare to the rest of the year.

So what’s an investor to do? Just be prepared to roll with an uptick in volatility, and don’t let seasonal trading influence your overall strategy.

Dr. Jason Van Duyn

Dr. Jason Van Duyn

586-731-6020

AQuest Wealth Strategies

President

Dr. Jason Van Duyn CFP®, ChFC, CLU, MBA is a Registered Representative with and Securities and Advisory Services offered through LPL Financial, a Registered Investment Advisor. Member FINRA & SIPC. The LPL Financial registered representative associated with this site may only discuss and/or transact securities business with residents of the following states: IN, IL, TX, MI, NC, AZ, VA, FL, OH and CO.

Dr. Jason Van Duyn CFP®, ChFC, CLU, MBA is a Registered Representative with and Securities and Advisory Services offered through LPL Financial, a Registered Investment Advisor. Member FINRA & SIPC. The LPL Financial registered representative associated with this site may only discuss and/or transact securities business with residents of the following states: IN, IL, TX, MI, NC, AZ, VA, FL, OH and CO.